- Call Today: (904) 438-8082 Tap Here to Call Us

Understanding the Coverture Fraction and Passive Appreciation of Non-Marital Property in Florida Divorces

Introduction

Property division in a Florida divorce follows the principle of equitable distribution, meaning that marital assets and debts are divided fairly, though not always equally. When one spouse owns non-marital property, such as a home or business acquired before marriage, disputes may arise over whether the other spouse is entitled to a portion of its increased value during the marriage.

Two key legal concepts—the coverture fraction and passive appreciation—help determine whether and how much of a non-marital asset’s growth becomes subject to division in a Florida divorce. This guide explains how courts apply these principles and what spouses need to know when dividing assets with mixed marital and non-marital components.

What Is the Coverture Fraction?

The coverture fraction is a formula used in Florida divorce cases to determine how much of an asset, such as a retirement account or home, should be classified as marital property when it was partially acquired before or after the marriage. This fraction helps courts allocate only the marital portion of an asset’s growth for division, while the non-marital portion remains separate.

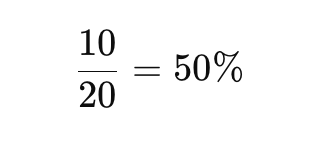

The formula is generally expressed as:

For example, if a spouse had a retirement account for 20 years but was married for 10 of those years, the coverture fraction would be:

This means that 50% of the asset’s value is considered marital property, while the remaining 50% remains non-marital and belongs solely to the original owner.

How the Coverture Fraction Applies to Retirement Accounts

The coverture fraction is often used when dividing pensions, 401(k)s, and other retirement benefits in a divorce.

- If contributions were made before the marriage, only the portion accumulated during the marriage is subject to division.

- The spouse who does not own the account may still receive a share of the marital portion through a Qualified Domestic Relations Order (QDRO).

- Courts use the coverture fraction to ensure the non-owning spouse only receives an interest in the portion of the retirement benefit earned during the marriage.

This formula prevents one spouse from unfairly benefiting from the other spouse’s pre-marital or post-divorce retirement contributions.

What Is Passive Appreciation in Florida Divorce Cases?

Passive appreciation refers to the increase in value of a non-marital asset due to market forces rather than direct financial contributions from either spouse. Common examples include:

- A home that increases in value due to rising real estate prices.

- A business that grows in worth due to economic conditions, rather than active efforts by the spouse.

- Stocks or investments that gain value due to market performance, rather than contributions from either spouse.

While passive appreciation alone is not considered marital property, Florida courts may treat a portion of the increased value as marital if marital funds or efforts contributed to the appreciation.

When Does Passive Appreciation of Non-Marital Property Become Marital?

Florida law considers passive appreciation partially marital when:

- Marital funds were used to pay the mortgage, taxes, or improvements on a non-marital asset.

- One spouse actively contributed to the asset’s growth, such as managing a business that was originally non-marital.

For example, if one spouse owned a home before the marriage but used marital income to pay the mortgage or renovate the home, the increased value due to those efforts may be considered partially marital.

The coverture fraction can be used in these cases to separate the marital and non-marital portions of appreciation.

Examples of Passive Appreciation and Marital Contributions

Example 1: Real Estate Appreciation

- A husband buys a home before marriage for $200,000.

- During the marriage, the home’s value increases to $350,000 due to rising market values.

- The mortgage was paid using both spouses’ income during the marriage.

In this case, part of the home’s appreciation may be marital property because marital funds were used to pay the mortgage. The court would calculate how much of the appreciation is due to market forces (non-marital) versus marital contributions.

Example 2: Business Growth During Marriage

- A wife starts a business before marriage, and it is valued at $100,000.

- By the time of divorce, the business is worth $500,000 due to increased market demand.

- The husband had no role in managing or contributing to the business.

Because the business grew primarily due to market forces and not marital efforts, the increased value would likely remain non-marital. However, if the husband helped manage the business, a portion of the appreciation could be considered marital property.

How to Protect Non-Marital Assets from Division in a Divorce

If a spouse wants to protect their pre-marital property from being classified as marital property, they should consider:

- A prenuptial or postnuptial agreement that clearly defines which assets remain non-marital.

- Keeping separate financial accounts and not using marital funds to pay for non-marital assets.

- Maintaining clear records of asset values before and during the marriage.

- Avoiding active marital involvement in the management or improvement of a non-marital asset.

Taking these steps can prevent disputes over whether an asset’s appreciation should be divided in a divorce.

How a Family Law Attorney Can Help

An experienced family law attorney can:

- Analyze whether passive appreciation of an asset should be considered marital property.

- Use financial experts to determine the coverture fraction for dividing retirement accounts or appreciating assets.

- Help protect pre-marital and non-marital assets in a divorce.

- Negotiate fair property division agreements that align with Florida law.

At Bonderud Law, we help clients navigate complex asset division issues, ensuring that marital and non-marital property is fairly and accurately classified. If you need assistance with property division in a Florida divorce, contact us today for a free consultation.

Conclusion

Florida courts apply the coverture fraction and passive appreciation principles to determine how assets are classified in divorce. While non-marital assets remain separate, any increase in value due to marital funds or efforts may be subject to division. Understanding these concepts can help spouses protect their financial interests and ensure fair asset distribution.

If you are facing a divorce involving businesses, real estate, or retirement accounts, consulting with an experienced attorney can help you navigate Florida’s complex property division laws.